Why Overly Confident U.S. Drillers Ditched Their Hedges

Some Big Oil companies are so confident that high oil prices are here to stay that they have completely ditched their hedges.

Scotiabank's Paul Cheng: the best hedge for oil and gas companies is a strong balance sheet.

U.S. shale producers will suffer a staggering $42 billion in hedging losses in 2022

Hedging is a popular trading strategy frequently used by oil and gas producers, airlines and other heavy consumers of energy commodities to protect themselves against market fluctuations. During times of falling crude prices, oil producers normally use a short hedge to lock in oil prices if they believe prices are likely to go even lower in the future. But with oil and gas prices recently touching multi-year highs, producers that typically lock up prices are hedging very lightly, or not at all, to avoid leaving money on the table if crude continues to soar.

However, failing to hedge adequately has its downside, as a recent Standard Chartered report reveals.

According to the commodity analysts, U.S. oil and gas companies are under-hedged for 2023, leaving them with unusually high price risk. This is a risky position to be in considering that the latest EIA data is bearish, with the inventory deficit relative to the five-year average at a 15-month low.

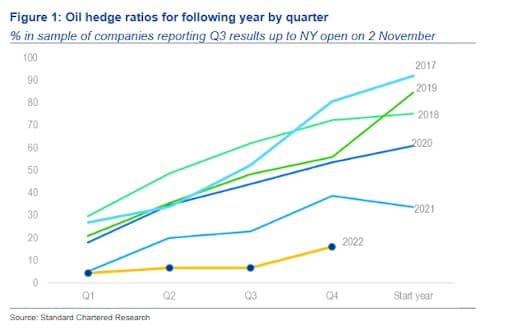

While only one-third of U.S. oil and gas companies have reported Q3 results as of November 2nd market open, Standard Chartered commodity experts warn that initial data covering some 1 million bpd of crude oil output, which includes the traditionally big hedgers, “their combined oil hedge book is now small at just 98mb, less than a fifth of the Q1-2020 peak of 563mb”.

“The most striking aspect of the data is how little is hedged for 2023,” Standard Chartered notes. “Within this sample, companies have a next-year hedge ratio of just 16%; a year ago the ratio was 39%, and in 2017 it was 81%.”

While the commodities experts view the U.S. oil industry as having grown cautious in its drilling policies, maintaining a strict discipline against relentless calls from the White House to produce more, they also say risk appetite is high–it’s just shifte

In fact, Standard Chartered says that the U.S. oil industry has become “risk-loving in terms of the price risk it is prepared to carry”.

“The lack of hedging for 2023 could be the result of an extremely bullish price outlook by oil executives, but we think current company exposure to price sits uneasily with the message of prudent and careful company strategy projected by many recent investor calls,” the report notes.

Source: Standard Chartered Research

The Best Hedge: A Strong Balance Sheet

Buoyed by the best financial performance in years, oil executives are wagering that high oil and gas prices are here to stay, with less hedging activity reflecting this optimism.

As Paul Cheng, an analyst at Scotiabank, has told Bloomberg, the best hedge for oil and gas companies is a strong balance sheet.

“Management teams have greater FOMO, or fear of missing out, being hedged in a runaway market. With prices rising and companies’ books stronger than they’ve been in years, many drillers are opting out of their usual hedging activity”, Cheng told Bloomberg.

Likewise, RBC Capital Markets analyst Michael Tran told Bloomberg, “Fortified corporate balance sheets, reduced debt burdens and the most constructive market outlook in years has sapped producer hedging programs.”

Some Big Oil companies are so confident that high oil prices are here to stay that they have completely ditched their hedges.

To wit, Pioneer Natural Resources Co .(NYSE: PXD), the biggest oil producer in the Permian Basin, has closed out almost all of its hedges for 2022 in a bid to capture any run-up in prices while shale producer Antero Resources Corp.(NYSE: AR) says it’s the “least hedged” in the company’s history. Meanwhile, Devon Energy Corp. (NYSE: DVN) is only about 20% hedged, way lower than the company’s ~50% normally.

Interestingly, some oil companies are being egged on by investors looking for more commodity exposure.

“It has been overwhelmingly the request of our investors. We have a stronger balance sheet than we’ve ever had, and we have more and more investors that want exposure to the commodity price,” Devon Chief Executive Officer Rick Muncrief has told Bloomberg News when asked about the decision to hedge less.

But the experts are now saying that the current trend of not hedging future output could have major implications up and down the forward price curve--in a good way.

That’s the case because energy producers act as natural sellers in futures contracts some 12 to 18 months ahead. Without them, trading in later months has less liquidity and fewer checks, leading to more volatility and potentially even bigger rallies. In turn, higher oil prices in the future are likely to encourage producers to invest more in drilling projects, a trend that had slowed down considerably thanks in large part to the clean energy transition.

Double-edged sword

Other than leaving money on the table, there’s another good reason why producers have been hedging less--avoiding potentially huge losses.

Hedging is broadly meant to protect against a sudden collapse in prices. Many producer hedges are set up by selling a call option above the market, a so-called three-way collar structure. These options tend to be a relatively cheap way to hedge against price fluctuations as long as prices remain range bound. Indeed, collars are essentially costless.

In theory, hedging allows producers to lock-in a certain price for their oil. The simplest way to do this is by buying a floor on the price using a put option then offsetting this cost by selling a ceiling using a call option. To trim costs even further, producers can sell what is commonly referred to as a subfloor, which is essentially a put option much lower than current oil prices. This is the three-way collar hedging strategy.

Three-way collars tend to work well when oil prices are moving sideways; however, they can leave traders exposed when prices fall too much. Indeed, this strategy fell out of favor during the last oil crash of 2014 when prices fell too low leaving shale producers counting heavy losses.

But exiting hedging positions can also be costly.

Indeed, U.S. shale producers will suffera staggering $42 billion in hedging losses in 2022, with EOG Resources (NYSE: EOG) losing $2.8 billion in a single quarter while Hess Corp. (NYSE: HES) and Pioneer paid $325M apiece to exit their hedging positions.

Whether or not this dramatic cut in hedging activity will come back to bite U.S. producers remains to be seen.